Everything You Need to Know About the Celtics Luxury Tax Maneuvers

On how the Celtics managed to get under the tax, what they get from it, and a creative plan to remain below it.

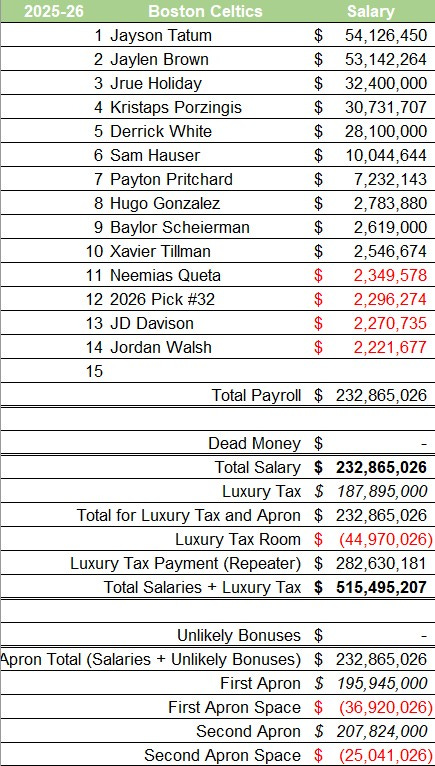

The Boston Celtics’ championship roster only played two seasons together. The rising costs to keep all their core players were unsustainable in the new salary cap environment. The new luxury tax modifications and apron penalties forced the Celtics to break up the team.

The 2025-26 Celtics would’ve cost over half a billion dollars to run back the roster. That’s why their offseason was all about subtraction. They traded Jrue Holiday for Anfernee Simons. They traded Kristaps Porzingis for Georges Niang, and then two second-round picks to get off him. The only other additions to their roster were minimum signings and their first-round pick (Hugo Gonzalez).

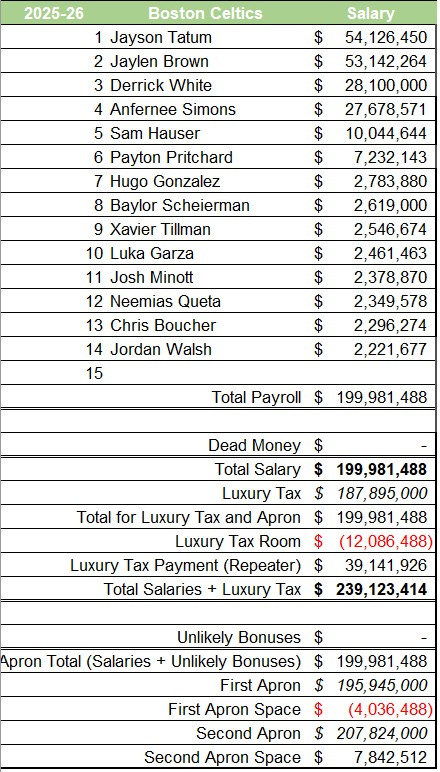

The Celtics managed to save over $200 million and get under the second apron threshold in the offseason. As a result, they won’t be prohibited from trading their 2033 first-round pick next season. The big penalty to disincentivize teams from exceeding the second apron is to “freeze” their first-round pick seven years in the future. They can’t trade their 2032 first-round pick since they finished last season over the second apron.

This felt like a recipe for a team to take a “gap year” and get a high lottery pick. Surprisingly, they’ve managed to stay at the top of the East and are currently tied for the second seed. But as great as their season has been, it doesn’t make sense to maximize the current season. They’re in all likelihood a second-tier championship contender even if Jayson Tatum comes back. They still should reduce their payroll and get under the luxury tax line.

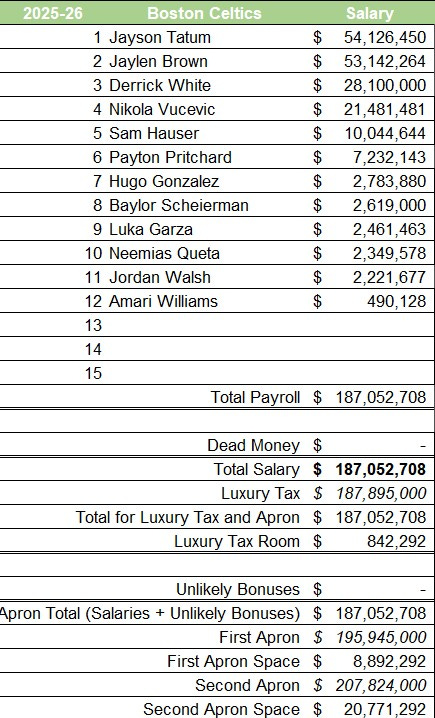

Yesterday, the Celtics pulled off what was considered impossible back in June 2025. They got under both the first apron threshold and the luxury tax line by trading Anfernee Simons for Nikola Vucevic, and trading Xavier Tillman, Josh Minott, and Chris Boucher without taking any salaries back.

Overall, the Celtics have saved a staggering $325 million between the beginning of the offseason and now. While the savings are nice, that’s not what this is about. They accomplish a couple of things here.

First, they can sign any player who gets bought out. Teams above the first apron aren’t allowed to sign players who make the $14.1 million non-taxpayer mid-level exception or more. Now that they’re no longer prohibited, they could theoretically sign a player like Khris Middleton or Jusuf Nurkic if waived.

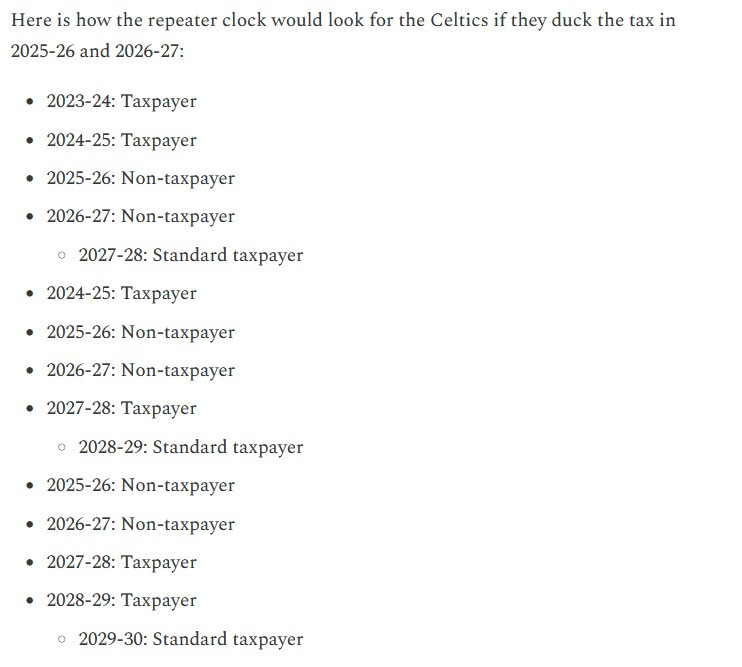

Second, and more importantly, they are one step closer to resetting their luxury tax repealer clock. Teams that are luxury taxpayers in three of the four previous seasons are designated repeat taxpayers. They have to pay $2 more per tax level than standard taxpayers, resulting in more punitive tax penalties. As an example, if the Celtics were standard taxpayers this season, their $283 million tax penalty shown above would be $193 million.

The Celtics need to avoid the luxury tax both in 2025-26 and 2026-27 to reset their repeater clock. Doing so would make them standard taxpayers from 2027-28, when Tatum will be two years removed from his injury, through 2029-30. This would give the Celtics a three-year window at the end of the decade to blow past the aprons and spend as much as possible. That is their true window to compete for a championship, not now.

This is a masterclass of salary cap management. But as great an accomplishment as it is, there’s another layer of planning the Celtics needed to consider ahead of time: filling up the rest of the roster without exceeding the tax line.

There are several minimum roster spot requirements teams must adhere to. For the most part, teams are required to have at least 14 players signed to standard contracts. There are exceptions to this rule. But in the immediate term, teams can never have fewer than 12 players signed to standard contracts at any time.

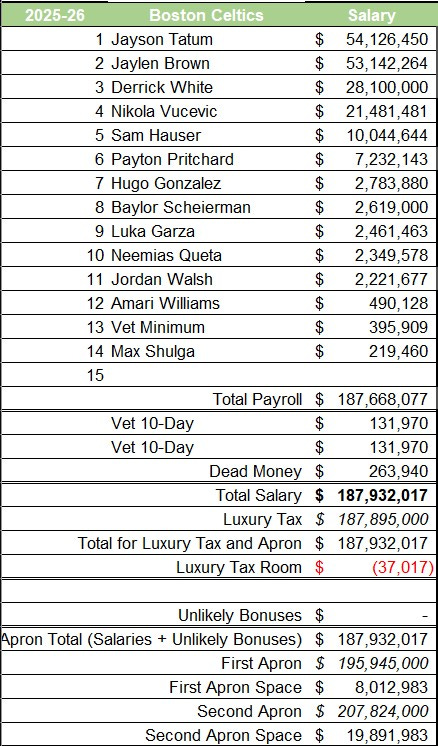

The Celtics were $1.3 million under the luxury tax threshold with just 11 players after trading Tillman, Minott, and Boucher. So they filled their 12th roster spot with Amari Williams, their 2025 second-round selection who was on a two-way contract. They chose him over a veteran because he costs less on their cap sheet than any other player.

Players who sign minimum-salaried contracts mid-season don’t get the full amount. They get a prorated amount based on the exact day they sign their contract. So instead of the veteran minimum for most players counting as $2,296,274, a player signed on the trade deadline would only get $884,197.

Williams’ minimum salary is smaller than that. The minimum salary for rookies this season is $1,272,869, while the prorated rookie minimum on the trade deadline was $490,128. The only reason Williams counts as that amount is that he was a Celtics draft pick. A player signing a standard contract with his draft rights, or from a two-way contract that was signed with his draft rights, counts on the drafting team’s cap sheet as the rookie minimum.

This wouldn’t work with any other rookie they sign as a free agent. There would be a tax variance credit that would treat the player on the Celtics’ cap sheet as if he were a veteran. He’d get paid $490,128 but count as $884,197 against the tax and apron.

As a result, the Celtics are currently $842,292 under the luxury tax line with 12 players. Now they’re allowed to wait two weeks before signing two players to reach 14 players. Teams are allowed to remain under 14 players for a maximum of 14 consecutive days and a total of 28 days in the entire regular season.

In two weeks, the veteran minimum will be reduced to $699,440, so that won’t be enough for two players. The rookie minimum will be $387,713. Even if they sign Max Shulga to one, their other rookie they have draft rights to, that wouldn’t be enough to pair with a veteran minimum while staying under the tax.

The alternative is to sign two players to 10-day contracts. Teams looking to stay under the tax post-trade deadline, like the Celtics are doing right now, typically sign players to 10-day contracts to fulfill minimum roster requirements. The idea is that by waiting two weeks, signing two 10-day contracts, then waiting another two weeks, teams stretch enough time that the prorated minimum salaries they eventually have to sign are as little as possible.

A 10-day contract this season for veterans is $131,970. The Celtics would effectively be charged that amount twice on their cap sheet between now and March 14, the day when the Celtics’ 28 “under-14” days would run out.

However, that’s still not enough. The two 10-day contracts and two rest-of-season veteran minimum signings, which would cost $395,909 each, leave the Celtics just $213,466 over the tax line. Even if they give one of those spots to Shulga, who’d cost $219,460 instead, they’d still finish just $37,017 above.

They’re so close. If only they had another rookie they had draft rights to get around this…

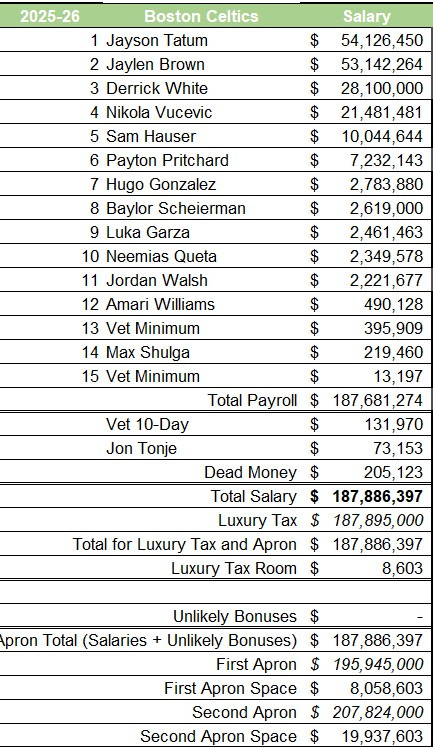

Enter John Tonje.

In the Celtics trade where they shipped Boucher and a second-round pick to the Jazz, you may have glossed over the fact that they got something in return. That something is two-way rookie Tonje, whom the Jazz drafted in the second round of the 2025 draft.

Although the Celtics didn’t draft Tonje, they inherited his draft rights in the trade. This makes the prorated rookie minimum applicable to Tonje as if they drafted him themselves.

As a bonus, and this is the key to this all, 10-day contracts for players signed via draft rights count as $73,153 as opposed to $131,970. However, this trick can only be used once since the team would no longer have the players’ drafted rights once the contract ends. If they wanted to give such a player another 10-day contract, he would get a tax variance credit, making it count as $131,970 on the team’s cap sheet.

This is the cleanest timeline for the Celtics to fill up their roster while remaining under the luxury tax line:

February 19 (14 days after the trade deadline): Sign a veteran 10-day ($131,970) and one of Shulga or Tonje to a rookie 10-day ($73,153).

February 28: 10-day contracts expire, go another 14 days under 14 players.

March 14: Sign a veteran to a prorated rest-of-season minimum veteran contract ($395,909) and the other of Shulga or Tonje, who did not get the 10-day contract earlier, to a rest-of-season minimum rookie contract ($219,460).

Then, on April 12, the final day of the regular season, sign any player to the 15th and final roster spot. This allows the Celtics to enter the playoffs with a full roster and just $8,603 below the luxury tax threshold.

The Celtics aren’t the first team to get under the luxury tax midseason and use cap gymnastics to finish the season below it. But what would make this timeline so unique is the implementation of a rookie signed to a 10-day contract without a tax variance credited to the team. I believe this would be a first in my eight years following the salary cap.

The other aspect that makes it so unique is how narrowly they avoid the tax. $8,603 is small, but surprisingly isn’t the smallest distance a team has finished below the luxury tax. Most recently, the 2022-23 Knicks finished just $1,553 under the luxury tax line after acquiring Josh Hart.

More on the 2026 Trade Deadline: Harden for Garland | Jaren Jackson Jr. Trade | Anthony Davis Trade | Two-Way Conversions and Buyouts | Zubac Trade Package | Warriors After Kuminga-Porzingis | Bulls Trade Deadline | Jared McCain Trade | Lakers Cap Space Plans | Magic’s Path Forward | Pistons, Spurs, Rockets Stood Pat

Unpacking the Jaren Jackson Jr. Trade

The NBA hit us with a flurry of trades on Tuesday. We are now at 7 trades, including the heavily rumored James Harden for Darius Garland swap that resulted in the Clippers receiving a second-round pick. This likely means the Cavaliers approached the Clippers about this first and were very out on Garland.

You can also see my work on:

Hey Yossi - maybe I'm missing something, but wouldn't it be better for Boston to use both 10-day contracts on veterans and then sign both rookies to minimum contracts? The value saved via the minimum contract for a rookie is more than the value saved via a 10-day contract for a rookie right?